Research

The Institute's faculty is a diversified international team of professors and researchers who are primarily dedicated to publishing cutting-edge research in top finance journals, but they also engage in high-level education in finance as well as in knowledge transfer activities such as conferences, seminars, and public debates on a broad range of finance topics.

Research video series

|

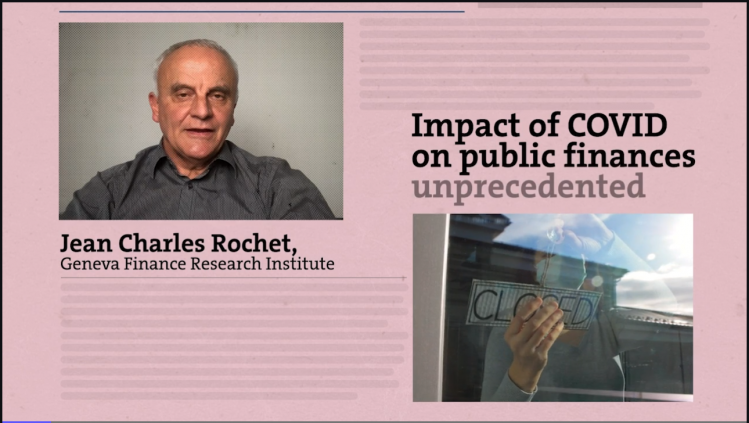

Sovereign debt sustainability in advanced economiesIn this video, Professor Jean-Charles Rochet presents his research on sovereign debt aimed at answering the following question: what is the maximum debt-to-GDP ratio that is sustainable by a government? 10 June 2021 |

|

|

Recent Publications

Berrada, T. N., Rindisbacher, M., & Detemple, J. 2025. Volatility During the COVID-19 Pandemic. Management Science.

https://doi.org/10.1287/mnsc.2024.04352

Derrien, F., Krueger, P., Landier, A., & Yao, T. 2025. ESG News, Future Cash Flows, and Firm Value?. The Journal of Finance.

https://doi.org/10.1111/jofi.13498

Shen, Y., Li, C., Scaillet, O., & Jiang, Y. 2025. Dynamic Portfolio Allocation under Market Incompleteness and Wealth Effects. Operations Research.

https://doi.org/10.1287/opre.2024.0976

Trojani, F., Quaini, A., & Korsaye, S. A. 2025. Smart Stochastic Discount Factors. Management Science.

https://doi.org/10.1287/mnsc.2024.05750

Ardia, D., Barras, L., Gagliardini, P., & Scaillet, O. 2024. Is it Alpha or Beta? Decomposing Hedge Fund Returns When Models are Misspecified. Journal of Financial Economics, 154, Article 103805.

https://doi.org/10.1016/j.jfineco.2024.103805

Dautović, E., Hau, H., & Huang, Y. 2024. Consumption Response to Minimum Wages: Evidence from Chinese Households. The Review of Economics and Statistics.

https://doi.org/10.1162/rest_a_01411

Hau, H., Huang, Y., Lin, C., Shan, H., Sheng, Z., & Wei, L. 2024. FinTech Credit and Entrepreneurial Growth. The Journal of Finance, 79(5), 3309–3359.

https://doi.org/10.1111/jofi.13384

Hau, H., & Ouyang, D. Can Real Estate Booms Hurt Firms? Evidence on Investment Substitution. Journal of Urban Economics, 144, Article 103695. https://doi.org/10.1016/j.jue.2024.103695

Krüger, P., Sautner, Z., Tang, D. Y., & Zhong, R. 2024. The effects of mandatory ESG disclosure around the world. Journal of Accounting Research, 62(5), 1795–1847.

https://doi.org/10.1111/1475-679X.12548

Menkveld, A., ... Scaillet, O., ... Zwinkels, R. 2024. Nonstandard Errors. The Journal of Finance, 79(3), 2339–2390.

https://doi.org/10.1111/jofi.13337

> For a complete list, please visit our Knowledge & Publications page.

Recent Ph.D. Theses

Empirical Essays on Regulatory Driven Bail-in Debt Instruments: the case of AT1/CoCoBonds (Kut, C. 2025)

The Stability of Financial Networks and Over-the-Counter Markets: Theory, Computation and Applications (Tywoniuk, M. 2025)

The Risk-Return Characteristics of Commercial Real Estate and Portfolio Implications (Johner, L. 2025)

Climate and Sovereign Debt Sustainability (Seghini, C. 2024)

Three Essays in Financial Economics (Maino, A. G. 2024)

Essays on Factor Models (Fortin, A. P. 2024)

Analyzing semi-variances at individual level: the pricing, risk premiums, and their relation to stock return (Anisimov, E. 2023)

Three essays on asset pricing and portfolio allocation (Auberson, M. 2023)

Essays in Asset Pricing (Korsaye, S. A. 2023)

Essays in International Finance and Monetary Economics (Terracciano, T. 2023)

Three Essays on Sustainable Finance (Jouvenot, V. 2022)

Three essays on Fintech and online marketplaces (Shan, H. 2022)

Three Essays on Corporate Finance (Zhang, Ye. 2022)

Real Estate Investments, Macroeconomic Risk Factors and Portfolio Implications (Delfim, J.-C. 2021)

Three Essays on Chinese Banking and Corporate Finance (Zhang, Z. 2020)

> Click here for more information on the Ph.D. in Finance program.